Economic Update | Mar 27, 2026

Hosted by Andrew Toccaceli, RICP®, MRFC® and Coley Neel, CFA® | W.A. Smith Financial Group

Get a clear look at what you’re paying and how much risk you’re taking. This complimentary review helps identify your portfolio’s costs, risk exposure, and opportunities to better align your investments with your goals — all with no obligation.

Get Started

Thank you to everyone who joined us for our Q1 2026 Client Connect. We covered a range of timely topics, from company updates and market conditions to thoughtful strategies for gifting and planning for future generations. If you were unable to attend, or would like a refresher, here is a summary of what we discussed.

We opened the session with updates on upcoming events and ways clients can stay connected throughout the year.

Our next Client Connect is scheduled for Wednesday, June 17, 2026, at our Sheffield Village Office (Lower Level). If there is a topic you would like us to cover in a future session, we welcome your input. You can share ideas by emailing Maddie at Maddie@WASmithFinancial.com.

We also shared options for clients who may want to introduce a guest to the firm.

One option is a series of educational dinner seminars, held on:

These sessions will focus on the four hidden drags on retirement and how to avoid them.

If you are interested in attending any of these events with a guest, you can contact Maddie at Maddie@WASmithFinancial.com or 1-866-417-4156, or reach out directly to your advisor.

We also shared a save-the-date for Thursday, August 6, 2026, for our annual Wish Upon a Star: A Night of Hope and Wishes event. More details will be shared as the event approaches.

We reviewed key themes for the start of 2026 and how these dynamics may carry out through the remainder of the year.

The discussion included a brief recap of market performance, along with potential actions by the Federal Open Market Committee (FOMC) and ongoing developments reflected in economic projections.

We also addressed the impact of geopolitical unrest and market volatility, noting that these factors have been present but not uncommon in broader market cycles.

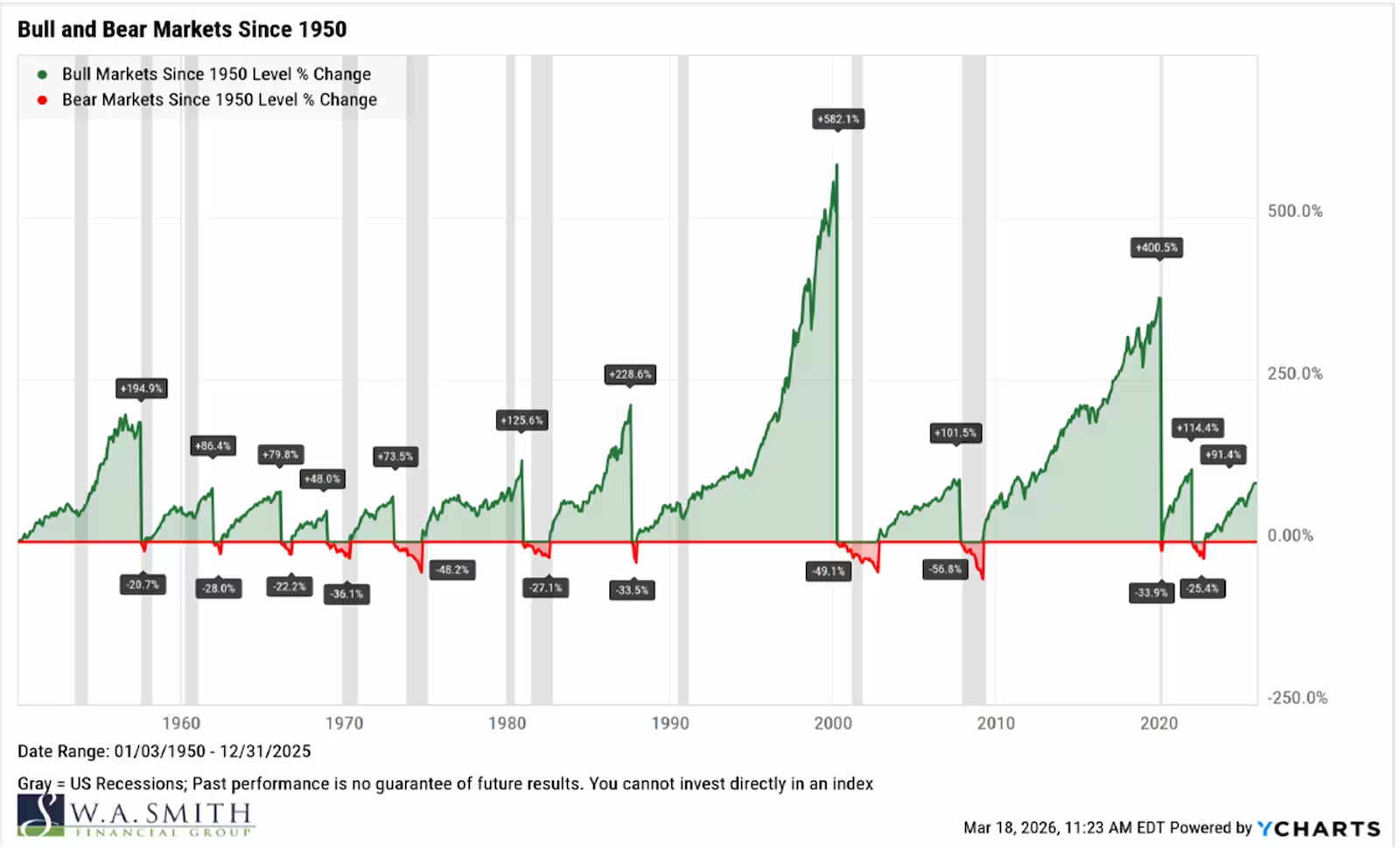

A central theme of the discussion was that fundamentals remain critical for stock selection, particularly in environments where market leadership can be concentrated.

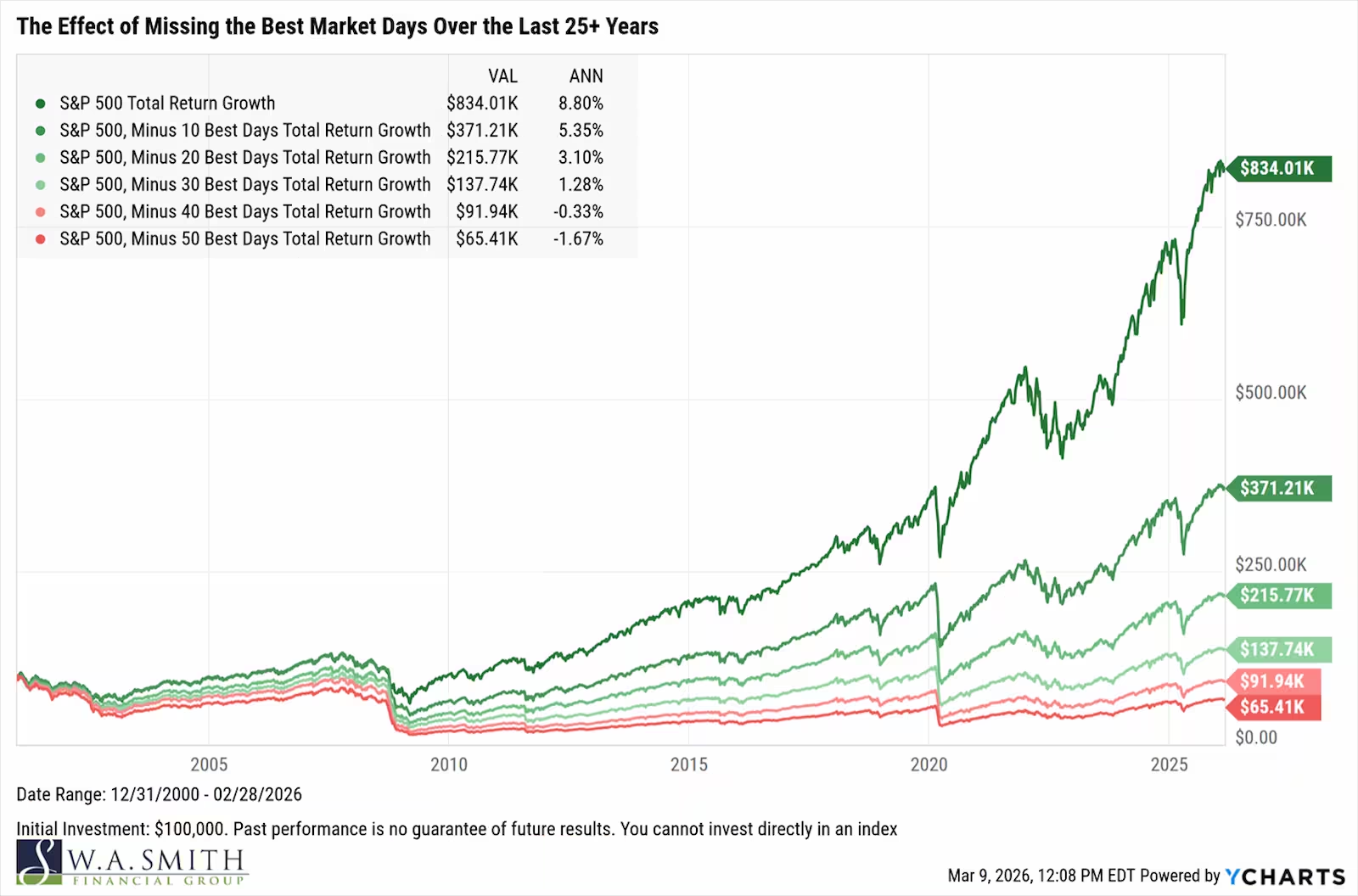

We also reinforced the long-term power of bull markets and the importance of remaining invested through periods of uncertainty. While short-term volatility can create discomfort, long-term market participation continues to be a key driver of outcomes for investors.

A significant portion of the Client Connect focused on strategies grandparents can use to support younger generations in intentional, tax-aware ways.

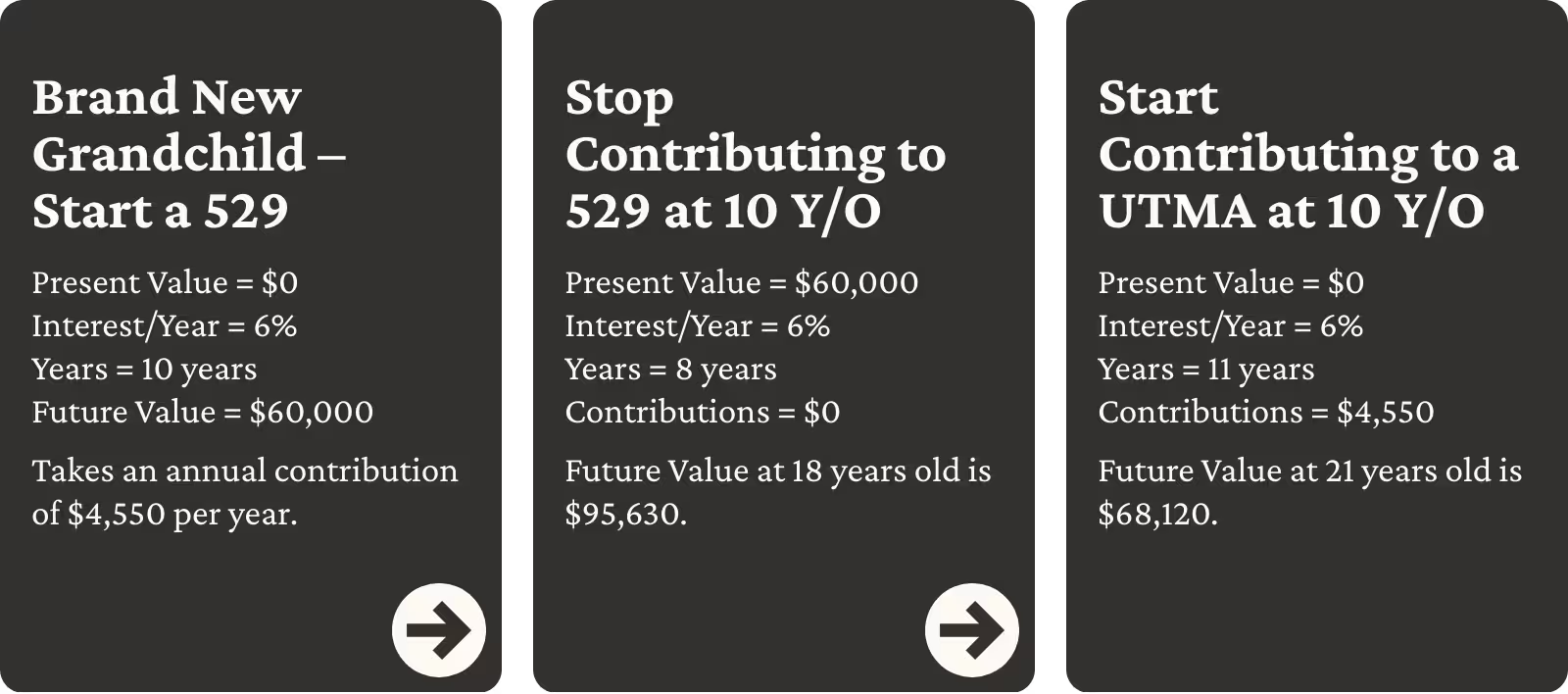

529 plans were discussed as a strong option for education-focused planning. These accounts allow for tax-deferred growth, with withdrawals generally tax-free at the federal level when used for qualified education expenses.

We walked through an example showing how contributing $4,550 per year for 10 years could grow to roughly $60,000, and how stopping contributions at age 10 could allow the balance to grow to approximately $95,630 by age 18.

UTMA and UGMA accounts were presented as a more flexible option for general-purpose gifting. Assets can be used for nearly any expense that benefits the child, such as education, weddings, first homes, vehicles, or starting a business.

We also shared how combining planning tools can be effective. Using a monthly contribution of approximately $379, a family could potentially build:

That totals roughly $163,750 per child, with the potential for significantly more if parents and grandparents coordinate their efforts.

We concluded the session with a discussion on broader gifting and charitable planning strategies.

Individuals may gift up to $19,000 per recipient per year without filing a gift tax return. The current lifetime gift and estate tax exemption is $15 million per individual. Gifts may be made using cash or assets, though the tax impact depends on the source of funds.

For individuals age 70½ or older, QCDs allow direct transfers from a traditional IRA to a qualified charity. These gifts can satisfy required minimum distributions while being excluded from taxable income, up to $100,000 per person per year.

DAFs allow individuals to make charitable contributions now and distribute funds to charities over time. Contributions may be made using cash or appreciated assets, with potential tax benefits in the year of contribution. Assets inside the DAF can be invested and may grow before grants are made, though contributions are irrevocable.

Life insurance was also discussed as a way to leverage annual gifts into a larger, tax-efficient benefit for children or grandchildren when structured appropriately.

If any of the strategies discussed here raised questions or sparked ideas, our team is happy to help. Whether you attended the event or are reviewing this recap for the first time, your advisor can walk through how these concepts may apply to your personal situation.

You’re always welcome to reach out to schedule a conversation or connect with our office for additional guidance.