Economic Update | Apr 14, 2026

Hosted by Andrew Toccaceli, RICP®, MRFC® and Coley Neel, CFA® | W.A. Smith Financial Group

Get a clear look at what you’re paying and how much risk you’re taking. This complimentary review helps identify your portfolio’s costs, risk exposure, and opportunities to better align your investments with your goals — all with no obligation.

Get Started

March was a bumpy month for investors. Rising tensions involving Iran sent oil prices sharply higher and rattled financial markets, reminding us how quickly geopolitical events can shift the investing landscape.

The S&P 500 finished the month slightly lower, and technology-heavy indices like the Nasdaq felt more pressure as investors moved away from higher-risk areas and toward more defensive parts of the market.

While the headlines were unsettling, it's important to keep perspective — the broader market remains in positive territory over the past year, and the fundamentals underpinning our strategies remain healthy.

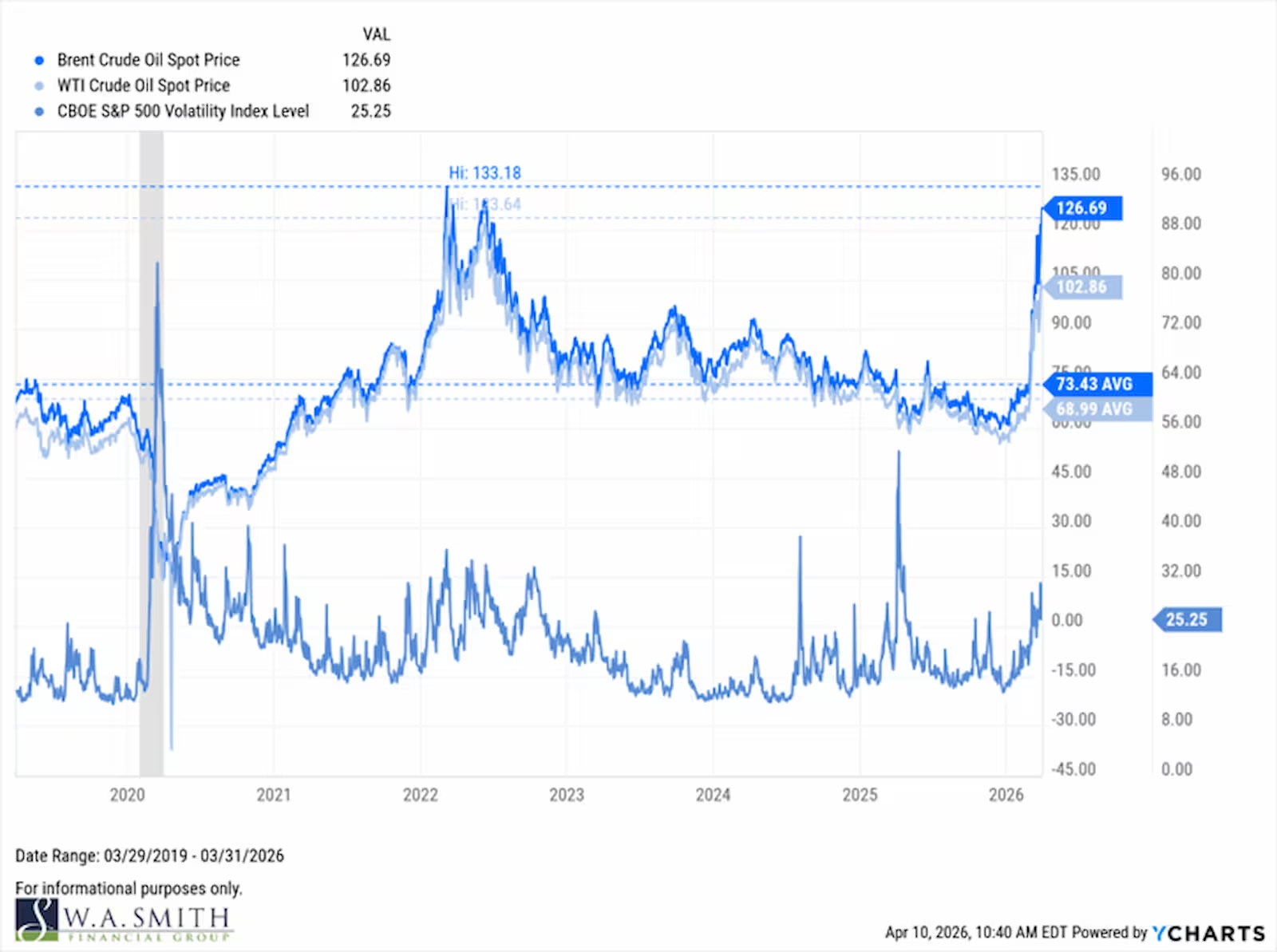

The escalation of conflict involving Iran was the primary driver of market volatility in March. As tensions intensified, oil prices surged — Brent crude climbed to roughly $127 per barrel and West Texas crude to around $114 — pushing U.S. gas prices to approximately $4.25 per gallon.

For everyday Americans, that shows up directly at the pump. For markets, higher energy prices bring renewed concerns about inflation and make the Federal Reserve's job of managing interest rates more complicated.

Market volatility, as measured by the VIX, rose alongside oil prices — a pattern we've seen before during geopolitical flare-ups in 2020 and 2022. In both of those cases, markets ultimately worked through the uncertainty. We're watching the current situation closely with the same long-term lens.

Not all areas of the market moved in the same direction in March, which is an important reminder of why diversification matters:

Over the past 12 months, however, most major market indices have remained solidly positive, putting March's pullback in proper context as a short-term speed bump rather than a change in direction.

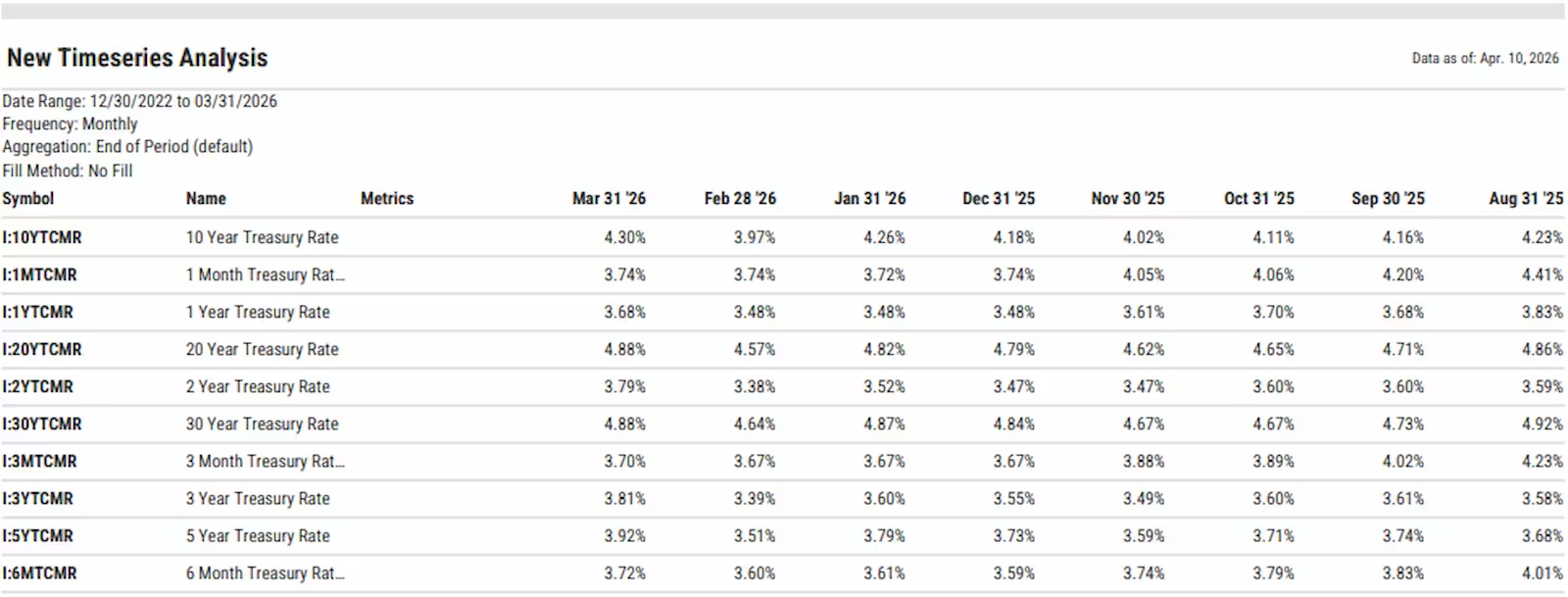

On the interest rate front, the yield curve, which had been inverted for much of the past two years, has now re-steepened to a more normal, upward-sloping shape.

The 10-year Treasury yield ended March near 4.30%, while shorter-term rates held around 3.7–3.8%. This shift creates better opportunities in intermediate-term bonds, and we continue to favor that part of the fixed income market over holding excess cash.

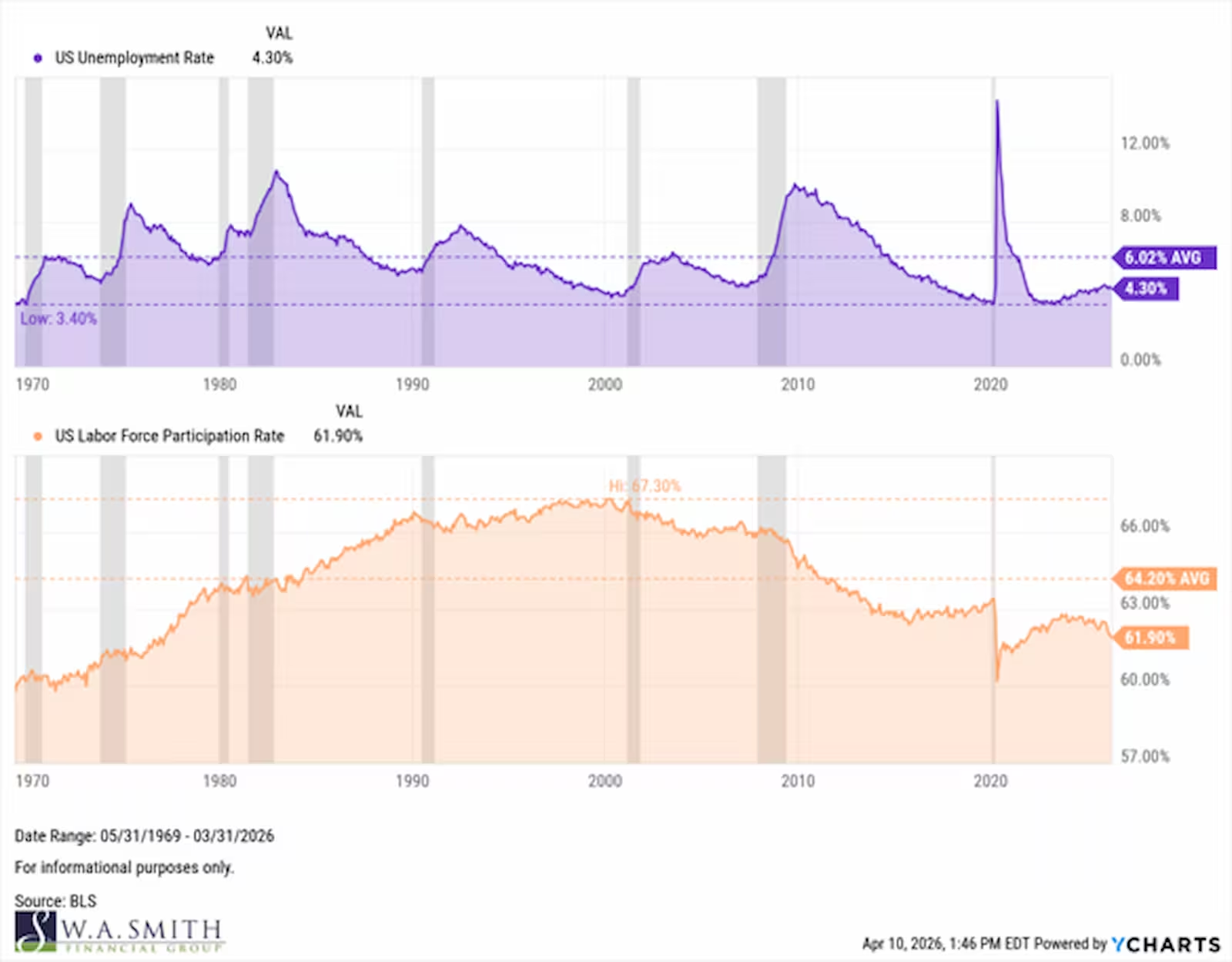

The broader economy also showed continued resilience in March. The unemployment rate remains low at roughly 4.3%, employers added approximately 178,000 jobs, and wages continued to grow.

These are encouraging signs that, despite the noise, the economic foundation is holding up. The primary risk to watch is whether sustained high energy prices begin to weigh on consumers and complicate the Federal Reserve's path toward eventual rate cuts.

The companies held across our multiple strategies continue to show strong balance sheets, solid cash flows, and durable earnings, exactly the qualities you want when markets get choppy.

Our Investment Committee is actively monitoring the situation involving Iran, energy prices, and Federal Reserve policy, and we'll continue evaluating our strategies using our disciplined, 5-step due diligence process.

As we have noted in the past, markets will always have moments of uncertainty, and March was a clear reminder of that.

But through it all, our focus will not waver. Despite the volatility in the markets, our focus remains on providing you with Financial Peace of Mind — keeping your long-term goals front and center, managing risk thoughtfully, and making sure you feel informed and confident every step of the way.

We hope you are enjoying the start of spring and look forward to seeing you again soon.