Economic Update | Mar 19, 2026

Hosted by Andrew Toccaceli, RICP®, MRFC® and Coley Neel, CFA® | W.A. Smith Financial Group

Get a clear look at what you’re paying and how much risk you’re taking. This complimentary review helps identify your portfolio’s costs, risk exposure, and opportunities to better align your investments with your goals — all with no obligation.

Get Started

Financial markets experienced increased volatility in February as investors navigated geopolitical developments, evolving economic data, and shifting expectations about monetary policy. After multiple years of strong market performance, the second month of 2026 introduced a more cautious tone as investors reassessed the economic outlook and the potential path of Federal Reserve policy. While market movements were uneven across sectors and regions, the broader economic backdrop remains resilient and continues to support constructive long-term fundamentals.

US equity markets finished the month modestly lower as investors digested rising oil prices, mixed economic data, and renewed debate surrounding the timing of potential interest rate cuts. The Nasdaq Composite underperformed as profit-taking continued within several mega-cap technology companies following a period of exceptional multi-year gains, particularly among artificial intelligence-related leaders.

At the same time, market leadership broadened across sectors and styles, with value-oriented and defensive segments, including energy, utilities, and materials, providing pockets of relative strength. This shift reflects a continued transition toward a more balanced market environment where diversification, earnings durability, and valuation discipline are becoming increasingly important for investors.

Economic data released during the month also contributed to a more cautious market environment. February’s Non-Farm Payrolls report came in weaker than expected, suggesting that labor market momentum may be gradually moderating following several years of exceptionally strong job growth.

Importantly, however, the broader labor market remains healthy. The unemployment rate remains historically low, wage growth continues to trend modestly higher, and labor force participation has stabilized. These trends suggest that the labor market may be transitioning toward a more sustainable pace of growth rather than signaling a meaningful deterioration in economic conditions.

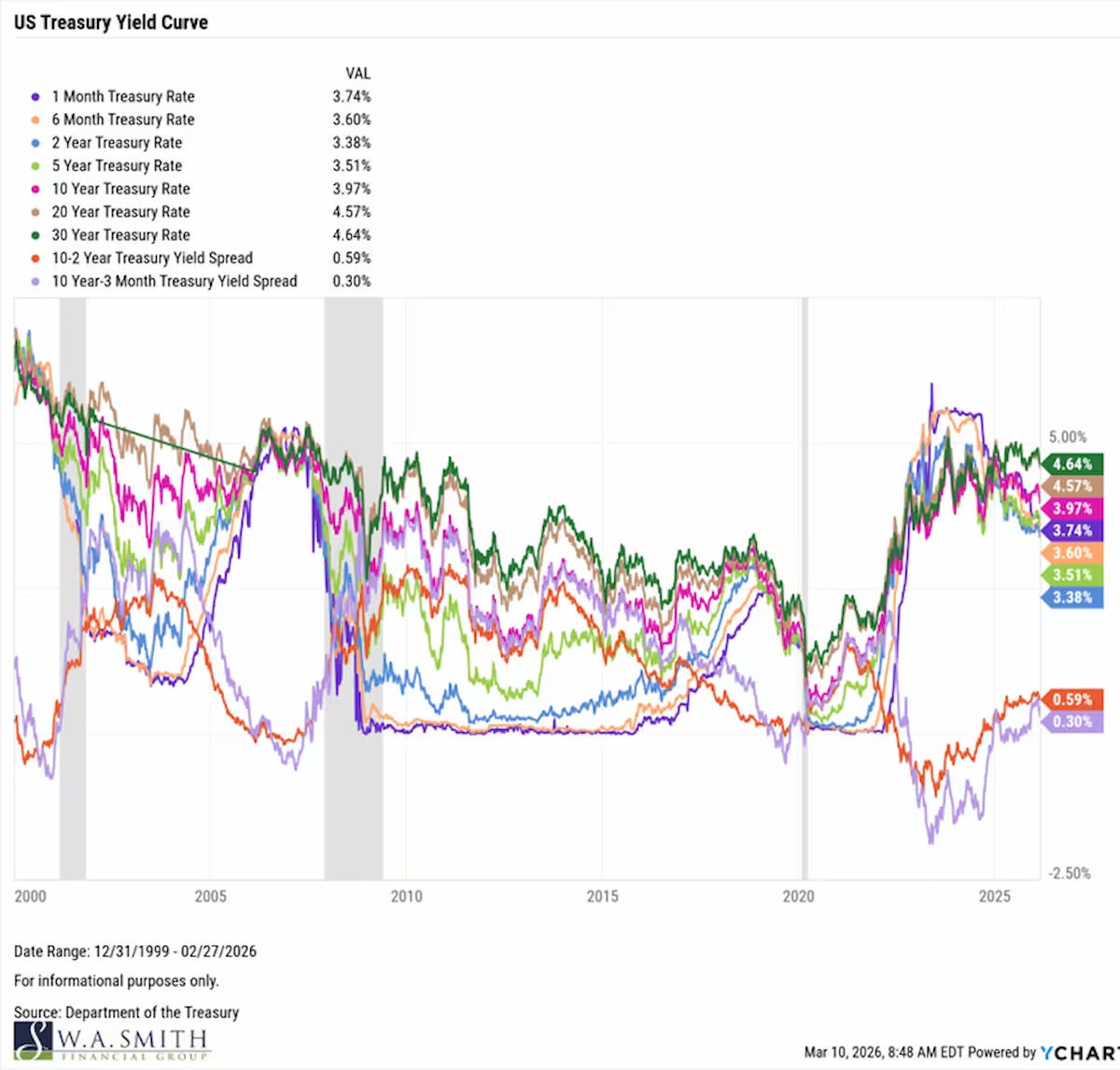

At the same time, Treasury yields moved modestly lower across much of the yield curve as markets began to price in the possibility of future Federal Reserve policy easing later in the year.

Another key development influencing markets in late February and early March has been the escalation of geopolitical tensions involving the United States, Israel, and Iran. The conflict has introduced an additional layer of uncertainty into global markets, particularly within energy markets, where concerns about potential disruptions to supply routes in the Middle East have pushed crude oil prices higher.

While energy prices have risen in response to these developments, they remain well below the peak levels experienced during the 2022 energy shock. Nevertheless, heightened geopolitical tensions can create volatility in commodity markets and may influence inflation expectations, consumer spending, and global economic growth if disruptions were to intensify.

At this stage, markets appear to be pricing in a geopolitical risk premium rather than a sustained supply disruption, but developments in the region remain an important factor for investors to monitor in the months ahead.

Despite the near-term volatility, several underlying trends remain supportive for long-term investors. Corporate balance sheets remain generally healthy, many companies continue to generate strong free cash flow, and earnings growth expectations remain positive across a broad range of industries.

Additionally, the broadening of market participation beyond a narrow group of mega-cap technology companies represents a constructive development. Value-oriented sectors, international equities, and small-cap stocks have increasingly contributed to overall market performance, creating a more diversified and balanced investment landscape.

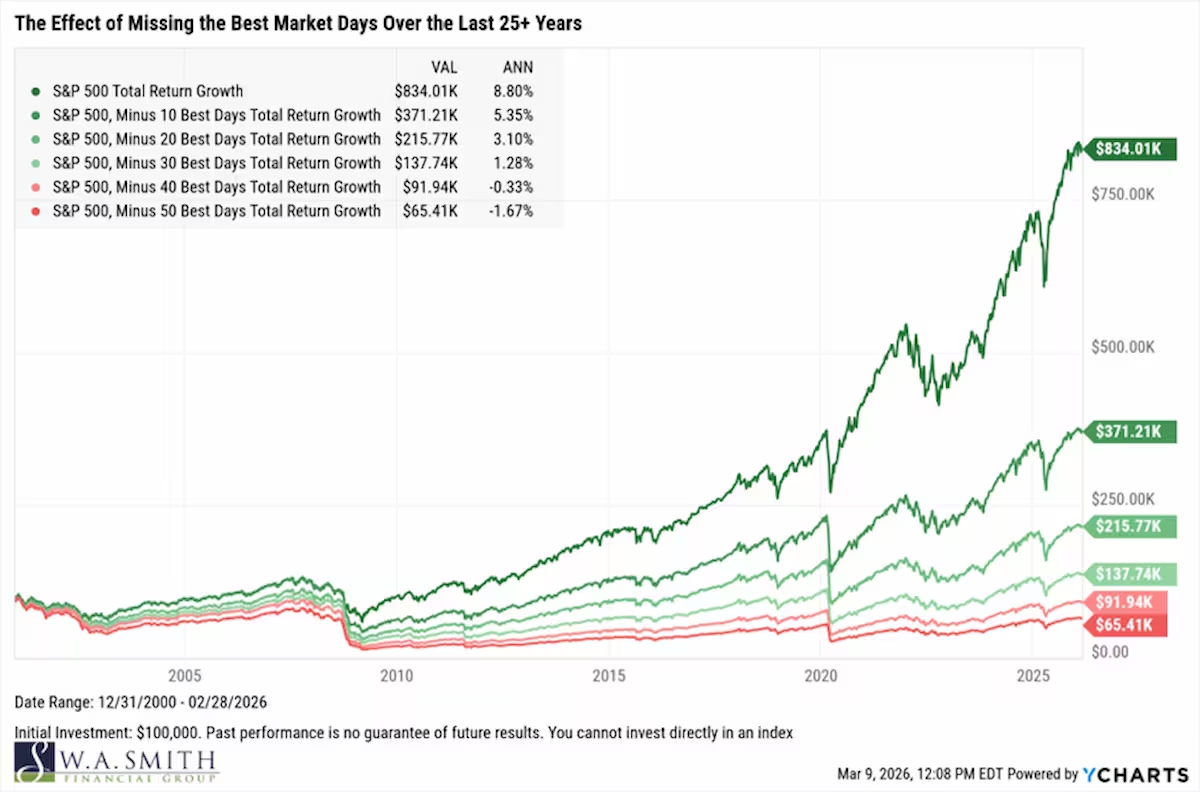

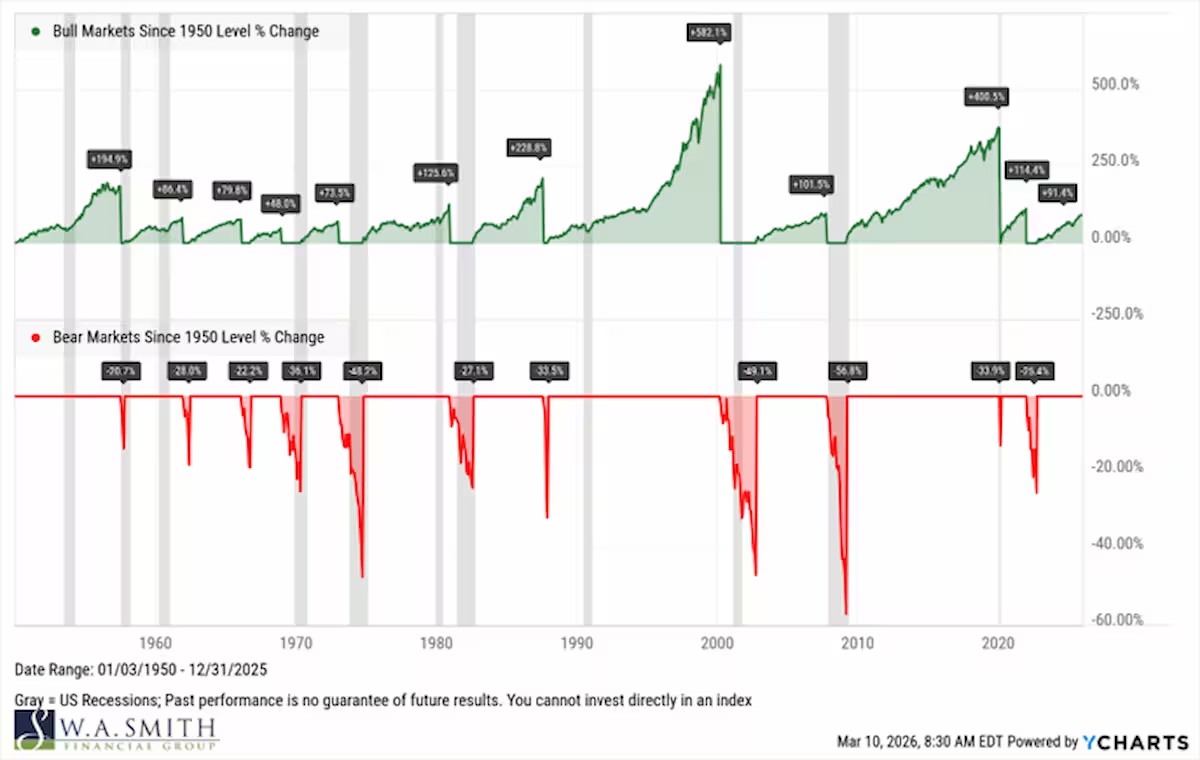

History also reinforces the importance of maintaining a disciplined long-term investment approach during periods of market uncertainty. While short-term volatility can be unsettling, market data consistently shows that missing just a handful of the strongest days of the market can significantly reduce long-term investment returns.

Likewise, bull markets have historically lasted longer and produced significantly larger cumulative gains than bear markets, underscoring the importance of remaining invested through market cycles rather than attempting to time short-term movements.

While geopolitical developments, economic data releases, and shifts in policy expectations may continue to drive short-term market fluctuations, our investment philosophy remains firmly grounded in the underlying fundamentals that support long-term wealth creation.

We continue to focus on companies with strong balance sheets, durable cash flow generation, and resilient earnings potential while maintaining diversified portfolios designed to navigate a variety of economic environments.

Most importantly, our primary objective remains unchanged: to help you achieve Financial Peace of Mind.

Market volatility is a natural and unavoidable part of investing, but our disciplined investment process and long-term perspective remain constant. We will continue to monitor the global markets and the economy and provide updates as warranted.

We hope that you are preparing for Spring, and we look forward to seeing you again soon!