Economic Update | Dec 11, 2025

Hosted by Andrew Toccaceli, RICP®, MRFC® and Coley Neel, CFA® | W.A. Smith Financial Group

Get a clear look at what you’re paying and how much risk you’re taking. This complimentary review helps identify your portfolio’s costs, risk exposure, and opportunities to better align your investments with your goals — all with no obligation.

Get Started

November marked a period of recalibration for U.S. markets as investors digested softer economic data, evolving monetary-policy expectations, and shifting sector leadership.

While headline index performance appeared muted, underlying market dynamics reflected a notable broadening of participation (aka, breadth) beyond the mega-cap growth names that had dominated much of the year.

The end of the prolonged U.S. government shutdown removed a significant source of uncertainty, restored the flow of official economic reports, and helped investors better assess conditions ahead of the December 9–10 FOMC meeting.

We must note, however, that much of the data that is coming out post the shutdown is likely dated and in need of an update.

That said, it is refreshing to finally start receiving new economic data.

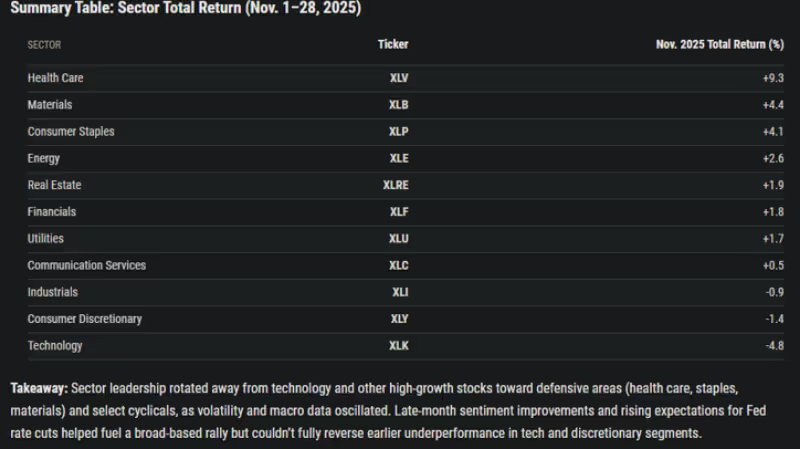

Equity returns were mixed but broadly stable.

The S&P 500 delivered a modest gain of +0.1%, extending its seven-month streak, while the Nasdaq Composite declined –1.5%, pressured by weakness in large-cap technology and AI-related names.

In contrast, defensive and income-oriented sectors posted strong results, with Health Care (+9.3%), Consumer Staples (+4.1%), and Utilities (+1.7%) leading the month.

This rotation suggests a more cautious tone as investors weighed slowing earnings momentum and uneven macro signals.

Small caps and international equities also improved, with the Russell 2000 up +0.96% and MSCI EAFE up +0.64%, indicating broader market participation.

Labor market developments confirmed a gradual cooling, consistent with the Fed’s objective of rebalancing supply and demand.

The unemployment rate held at 4.4%, labor force participation remained steady near 62.4%, and real hourly earnings rose modestly.

Private-sector hiring slowed, with the latest ADP report showing a 32,000-job decline, driven largely by small businesses.

While hiring momentum moderated, job losses remained contained, suggesting normalization rather than deterioration.

This cooling, in turn, reinforced expectations that the Federal Reserve will deliver another rate cut in December.

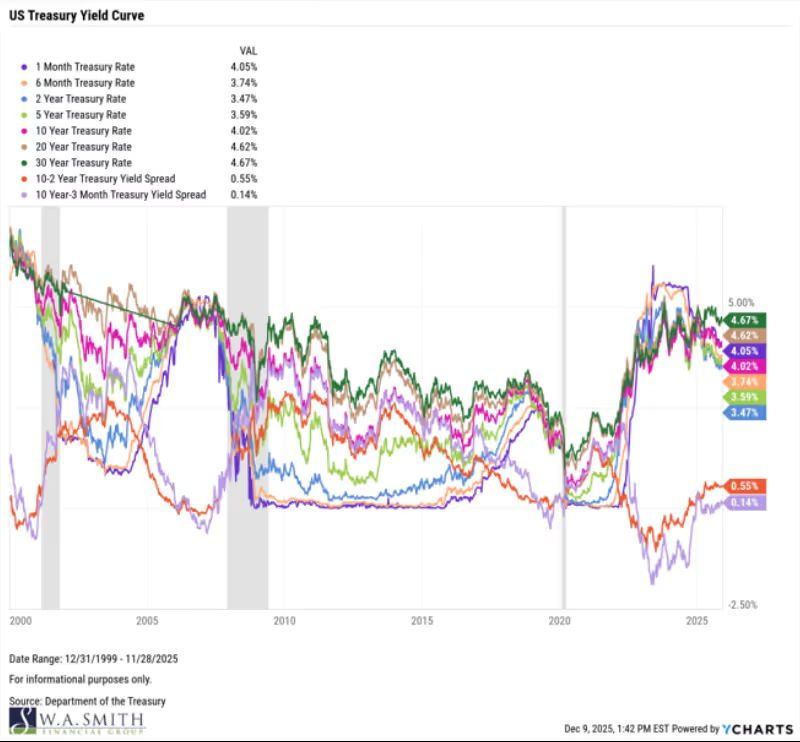

The bond market adjusted accordingly.

Short-term Treasury yields fell between 1–5 basis points across 1–12-month maturities, while intermediate yields declined 9–13 bps.

Meanwhile, the long end remained anchored, with the 20-year rate at 4.62% and the 30-year rate at 4.67%, reflecting stable inflation expectations and a persistent term premium.

These moves furthered the curve’s re-steepening trend:

The 10Y–2Y spread widened to +0.55%, and the 10Y–3M spread turned positive at +0.14%, signaling improving financial conditions and a market increasingly aligned with a soft-landing scenario.

Style performance shifted as well.

Value outperformed growth during November across both large- and small-cap segments, with Russell 1000 Value up +2.64% and Russell 2000 Value up +2.88%, while their growth counterparts declined.

Although growth remains the stronger performer over the trailing 12 months, supported by AI-related earnings strength, the style and sector rotation highlights investors’ renewed appreciation for quality, stability, and cash-flow resilience late in the economic cycle.

In summary, November was a month marked by normalization, characterized by cooling labor trends, steadier inflation dynamics, a gradually steepening yield curve, and more balanced equity leadership.

As the market turns toward the final FOMC meeting of the year, expectations for a December rate cut are high, but attention is shifting to how the Fed communicates the policy path for 2026.

Regardless of short-term fluctuations or macro uncertainty, our focus remains steadfast on providing you with clarity, confidence, and long-term financial peace of mind.

We wish you all the very best during the holiday season and look forward to seeing you in 2026!